With geopolitical instability, persistently high interest rates, tariffs and rising energy costs, the A/E industry, along with the overall U.S. economy, is certainly facing some significant headwinds. And yet, A/E industry results in 2025 generally were very strong, and year-end backlogs, along with business leaders’ sentiment, seem to point to continued growth in 2026.

Poll Results

We recently conducted an informal poll of client firms, including participants in our annual “A/E Business Valuation and M&A Transactions Survey,” to better quantify how firms performed in 2025 and where revenue is trending in 2026. This poll consisted of 53 companies across the United States, including engineering firms, architectural practices and environmental consulting firms, with many responding firms offering multiple service disciplines.

Respondents reported that net service revenue levels in 2025 were up 11.5 percent overall (weighted by dollar volume). Engineering firms saw the strongest revenue growth at 13.3 percent, followed closely by environmental consulting firms at 13.0 percent, with architecture firms growing at a sub-inflationary rate of 2.7 percent.

Backlog growth suggests good prospects for continued growth in 2026. Respondents reported that overall backlog levels were up 28.7 percent year-over-year. Again, engineering firms led with a backlog increase of 32.7 percent, followed by architectural firms with a 23.5 percent increase and environmental firms with an 8.2 percent increase.

Surveying Sentiment

While this informal survey had a small sample size, the data are supported by a recently released report from the American Council of Engineering Companies Research Institute (ACEC-RI). Its “Engineering Business Sentiment Report” (iimag.link/ISzkg) uses a scale of zero to 100, positive or negative. The sentiment rating is calculated by subtracting the percentage of negative responses from the percentage of positive responses; a positive number indicates optimism, and a negative number indicates pessimism.

ACEC-RI’s First Quarter 2026 report indicates that overall sentiment regarding the U.S. economy was positive at 45 (up from 34 at the 2025 year-end). Interestingly, the same respondents rated the outlook for the engineering industry as a whole at a positive 76, and a positive 82 for their own respective firms.

In terms of specific markets, sentiment ratings reflect that a major driver of recent and anticipated growth has been the activities of the AI hyper-scalers (e.g., AWS, Google, Microsoft, Meta, etc.) and the direct and indirect demand for architecture, engineering and environmental services they’re creating. Data center construction obviously involves sophisticated MEP engineering services among other disciplines, but it also creates demand for energy production and distribution, water supply, wastewater management, and related environmental-compliance services.

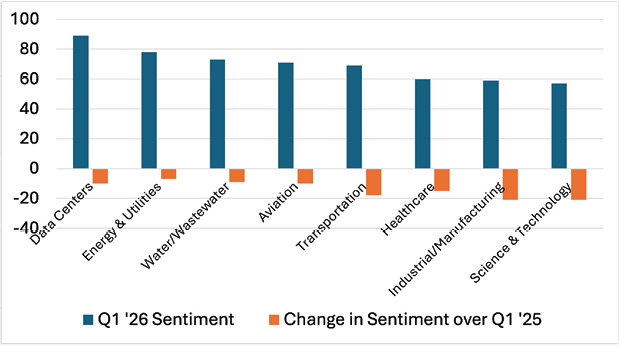

Below are the top-ranked market sectors from the latest ACEC-RI Business Sentiment report. As the chart shows, Data Centers, Energy and Utilities, and Water/Wastewater were the leading sectors by business sentiment, with ratings of 89, 78 and 73, respectively.

Source: ACEC Research Institute Engineering Business Sentiment © | 2026 Q

This raises the question of whether the rapidly growing data-center sector is masking a slowdown in other private- and public-sector development markets. For several years, the A/E industry has benefited from the $1.2 trillion Infrastructure Investment and Jobs Act (IIJA). But most of this federal funding has now been allocated, and authorization for the remaining funds expires in September 2026. According to the ACEC-RI report, uncertainty over the slow rollout of a new infrastructure spending bill was among the top concerns for business leaders, affecting their confidence in the industry’s economic outlook. Other top concerns included the political environment, general economic uncertainty, inflation and rising costs, tariff impacts, and recession concerns.

Despite these concerns and the growing economic headwinds, the A/E and environmental consulting industries have remained resilient and appear on pace for another year of growth in 2026.

Ian Rusk

Ian Rusk, Managing Principal of Rusk O’Brien Gido + Partners, has spent the last 20 years working with hundreds of architecture, engineering and environmental-consulting firms large and small throughout the United States and abroad, with a focus on ownership planning, business valuation, ESOP advisory services, mergers and acquisitions, and strategic planning.

Video: New Roundabout Under Construction at McIver and Old Florence Roads in Darlington County

Promenade at The Point

June Issue 2026

.jpg?width=225)