Back in 2021, I authored a column titled “How Private Equity Is Quietly Transforming the A/E Industry.” My goal back then was to describe and justify the factors driving outside investor interest in our sector and why so many design leaders initially seemed receptive to it. The marriages seemed a bit unconventional. Cerebral, creative and technical architects and engineers joining forces with financiers and dealmakers. And while other executives viewed this with a mix of curiosity and skepticism, the big question was whether this trend, still in its early innings, was sustainable? Well, five years later, the answer is a resounding “yes.”

Accelerating Acquisition

In fact, this decade has seen professional-services companies of all stripes being swept up by private-equity investment. Accounting firms, medical and dental practices, wealth-management providers, recruiting/placement specialists, and strategy and marketing consultants have all teamed up with financial sponsors for exit-strategy purposes.

The trickle of sellers that kicked off this movement has since become a torrent as the pace of deals has broadened and accelerated. In the last five years, the A/E industry has witnessed more than 100 firms take the private-equity route through various models. Companies across every discipline and geography; ENR 500 firms as well as those that aspire to be.

Rather than seeing failed outcomes and incompatible partnerships, the model’s success has emboldened an industry open to change. A/E leaders who could’ve sold to publicly traded companies or large, privately held strategics—or even implement ESOPs—changed course with a profound, new option in front of them. The lure of selling at an attractive EBITDA multiple, with the prospect of future growth and arbitrage ahead of the next recapitalization event, has proven too good to pass up.

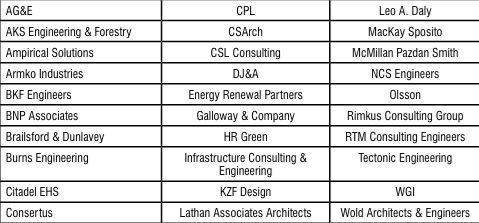

Select New A/E Firm Private-Equity Recapitalizations: 2024 to Present

The thesis driving soaring transaction volumes remains the same. Private-equity firms invest in established companies and seek higher returns on behalf of their limited partners, such as family offices, high-net-worth individuals, pension funds, endowments and foundations. They understand the attractiveness of our industry’s macro forces such as infrastructure renewal, environmental concerns, insatiable power/energy needs and facility modernization. To them, it’s another highly fragmented industry ripe for consolidation, led by professionals with limited transition or succession options. Investors also like design firms’ cash-flow generation and debt capacity as well as their incredible scalability.

Evolving Strategies

What has changed somewhat during the last five years is the investment strategy being employed. Early on, it was the sizable design firm ($50 million to $100 million-plus revenue) that was being recapitalized. It kept its brand, services and overall principles and culture. It was utilized as the sole platform for bolt-on acquisitions to scale and diversify. And while those still are sought after, today’s lower-middle market investors have acquired much smaller A/E firms, often with less than $20 million in revenue.

Others have adopted the “family of brands” approach. This involves acquiring disparate, smaller consulting firms ($5 million to $25 million) across the country and slowly bringing them together under a common holding company and identity. This model typically brings in an external, experienced industry leader to steer the entire ship.

Other observations and takeaways include the following:

1. Buy or build tailwinds. To be sure, private-equity partners can help accelerate growth by scooping up other firms. Dozens of private-equity-backed firms have been some of the most aggressive acquirers during this “M&A Supercycle” era. But not all of them have been. With impeccable timing, financial sponsors have been fortunate to see the A/E industry generate its strongest organic growth rates since the mid-2000s. With backlogs at record levels, many organizations have flourished by steadily achieving annual growth rates of 10 to 20 percent and sidestepping the integration challenges that come with serial acquisitions.

2. The benefits of an external perspective. One of the refreshing attributes private-equity groups can bring is a true outsider lens to a business. And why not? These groups invest in a variety of industries, including manufacturing, energy, logistics, retail and software. Company challenges can be universal and relatable. Some A/E CEOs have shared that leveraging experiences and best practices with other portfolio CEOs has been helpful, enabling them to challenge historical A/E “groupthink” dynamics. Private-equity investors can leverage case studies and new ideas to coach, plan strategically, train and test, manage finances, and develop businesses. In addition, many are seizing the opportunity to widely incorporate AI for value creation and as a competitive differentiator.

3. Ready, set, exit. Private equity has a preferred investment horizon (3 to 5 years, more or less) when they acquire and grow a company before selling it and returning capital (with returns) back to their limited partners. In most cases, this occurs in a secondary sale, with ownership transferred to another financial sponsor. Already, we’ve seen numerous A/E firms that initially recapitalized in the 2019-2022 period find homes with new partners. Less common have been sales to publicly traded firms or mergers of two private-equity-backed firms. Timing and market conditions are always unpredictable. And with an overhang of A/E investments today, it’s worth asking whether that could result in stalled exits, liquidity setbacks or value dilution.

4. More deals to come? Are there more private-equity investments looming on the horizon? Yes, obviously, discussions are ongoing between parties, and it’s unlikely we’re in the final stages of this cycle. On the other hand, how many more will occur is a bit nebulous. Keep in mind that a good number of ENR 500 firms are already with financial partners, and many others on that list are perfectly satisfied with their independence and path. Some firms with legacy or mature ESOPs could find an organizational reset appealing. Today, we’re also observing a new, younger generation taking over the C-suites at design firms everywhere. Our hunch is that these individuals may be more interested in maintaining control and independence than selling out to buyers or investors.

A great aspect of the A/E industry is that it encompasses a “big tent” of diverse ownership models—from sole owners and partners to ESOPs, family businesses, widespread shareholder groups and publicly traded companies. Each has its unique benefits, and ultimately, there’s no direct correlation between a firm’s ownership structure and its financial performance. This decade, private equity has emerged as a viable option for many firms, but it’s not for everyone. It is, however, here to stay.

Steve Gido

Steve Gido specializes in corporate financial advisory services, including mergers and acquisitions, business valuations, ownership transition plans, and strategic planning for engineering, architecture, environmental consulting and construction firms. He leads ROG+ Partners’ merger and acquisition practice, and has advised on a wide number of A/E/C transactions, representing buyers and sellers of all sizes and disciplines.

Video: New Roundabout Under Construction at McIver and Old Florence Roads in Darlington County

Promenade at The Point

June Issue 2026

.jpg?width=225)