APAC Will Lead Global Wind Gearbox and Direct Drive Equipment Markets Over Next Four Years, Says GlobalData

Asia-Pacific (APAC) is expected to lead the global wind gearbox and direct drive equipment markets with a share of 46% and 53.5%, respectively over the forecast period (2018–2022), says GlobalData, a leading data and analytics company.

The company’s latest report, ‘Wind Gearbox and Direct Drive, Update 2018’, reveals that the global trends of wind power are creating business opportunities for new and refurbishment markets. It states that prominent markets such as China, the US and EU, which had made significant strides in the wind market, are creating a significant market for gearbox refurbishments.

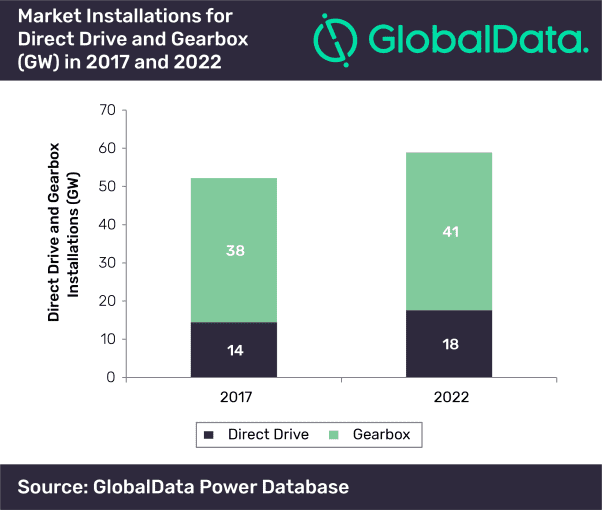

Installation of wind gearboxes and direct drive equipment are estimated to aggregate 209.6 gigawatt (GW) and 81.3GW, respectively over the forecast period.

The total installation of wind gearboxes stood at 37.8GW in 2017 as compared to 14.4 GW for direct drive, and will continue leading the market over the forecast period. However, due to their improved mechanical design, superior operation and maintenance aspects, direct drives are likely to experience a higher growth rate over the forecast period. The direct drives market is expected to witness 17.6GW of installations, i.e., 29.9% of the total installation in 2022.

Nirushan Rajasekaram, Power Analyst at GlobalData, says: “Within APAC, major countries such as China, India, Australia and South Korea are likely to boost the growth of the drive-train markets. The market for wind gearboxes in APAC is expected to reach to $1.58bn in 2022.”

China accounted for 27.3% of the global gearbox market value in 2017. The country is committed towards developing its renewable portfolio to sustain development activities and growing electricity demand from the transport sector industries and rural regions to improve standards of living, while reducing power sector emissions. However, the market is projected to decline till 2022, due to change in awarding wind projects from a feed-in tariff model to auctioning model.

Rajasekaram adds: “The historical installations of wind turbines in China will see the gearbox refurbishment market value grow significantly over the forecast period. India is estimated to be the fastest growing market for gearbox, growing at a CAGR of 15.9% over the forecast period. Similar to China, the government proposed ambitious renewable energy targets, which are expected to drive the wind equipment market. It is likely that direct drives will also see higher rates of deployment in India, during the forecast period.”

However, despite strong projections for wind gearbox and direct drive markets, certain market uncertainties exist. Major countries such as China, the US and Germany are experiencing slowdown in wind turbine installations, which would directly impact the drive-train market, although opportunities for refurbishment are plenty, owing to their legacy wind turbine installations.

Rajasekaram concludes: “Evolving power and smart technologies could result in wind power becoming uncompetitive and thereby impact its growth in the future. Emerging markets will require the construction of sufficient grid infrastructure to support new generation capacity addition, which could slow market deployment of wind power.”