Cement Companies Must More Than Double Efforts to Meet Paris Climate Goals

April 9, 2018, London: A new report ‘Building Pressure’ analysing 13 of the world’s largest publicly-listed cement companies reveals that they need to more than double their emissions reductions if they are to limit global warming to below two degrees, as agreed in the Paris Climate Deal. The companies analysed in the report from CDP – voted no. 1 climate change research provider by institutional investors[1] – have a total market capitalization of US$150 billion and represent 16% of global cement production. The cement sector itself accounts for 6% of global CO2 emissions.

Cement is the second most polluting industrial sector and is used in concrete, which after water is the most consumed product in the world. The built environment, which includes offices and residential buildings, uses concrete extensively and accounts for over a third of global emissions[2]. Regulation of the sector so far has been light but rising ambitions for low carbon cities and tightening building regulations could drive change up the chain.

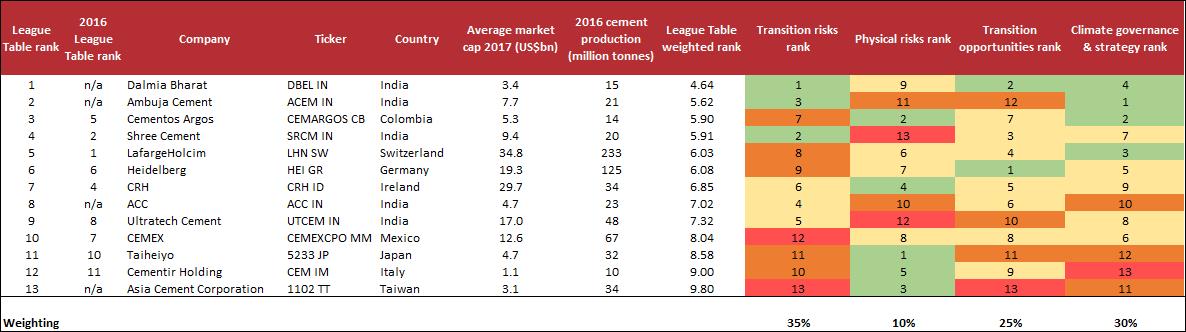

Indian companies top the CDP league table thanks to reducing their carbon footprint during the cement making process, in part due to better access to alternative materials[3] from other carbon intensive sectors. They also benefit from newer and more efficient cement plants driven by high market growth in the region, in contrast to their European peers that rely on older cement plants.

Paul Simpson, CEO of CDP commented: “Cement is a heavy and largely invisible polluter, yet taken for granted as a necessary building block of basic civilization. With potential pressure coming from multiple sources, including down the value chain in the form of building and city regulation, cement companies need to invest and innovate in order to avoid impending risks to their operations and the wider world. This may seem challenging at first, but every year it is delayed, the cost becomes greater, so management teams, regulators and investors need to think long term. There is a solution - cement companies just need to invest properly in finding it.”

There are however opportunities for companies who act early on climate risk. Companies can reduce costs by making their cement plants more energy efficient and secure their position in future sustainable cement markets by investing in low-carbon products. Governments can facilitate the development of these markets through regulation and incentives.

The report also highlights other potential risks and opportunities for the sector:

The CDP report assesses companies across four key areas aligned with the recommendations from Mark Carney’s Task Force on Climate-related Financial Disclosures (TCFD). As the TCFD recommendations become mainstream, investors will increasingly expect cement companies to disclose how they are adjusting their business models to manage transition risks, while taking advantage of the opportunity to generate revenue from the global transition to a low-carbon economy.

CDP’s summary League Table for cement companies is below:

Marco Kisic, Senior Analyst at CDP commented: “Cement companies have made some progress towards reducing their emissions, but they need to do a huge amount more. It is clearly a complicated story because of our global reliance on cement, and the inherent emissions of the sector, but there are things that can be done. Cement companies should be looking at ways to further use alternative materials and fuels, improve the energy efficiency of their plants, and accelerate investments in low-carbon technologies such as carbon capture and storage, which is crucial for their long-term viability. Regulation may be the key driver for change here, and interestingly this may come from downstream as building regulators and owners shift their focus from operational emissions, to those associated with creating the buildings themselves.”

Anhui Conch, Siam Cement, Dangote Cement and China National Building Materials did not respond to CDP’s 2017 climate change questionnaire and are therefore not included in this report. We encourage investors to raise this lack of transparency in discussions with company management.

You can view the executive summary of the report here.

About CDP and this report

About CDP

CDP is an international non-profit that drives companies and governments to reduce their greenhouse gas emissions, safeguard water resources and protect forests. Voted number one climate research provider by investors and working with institutional investors with assets of US$87 trillion, we leverage investor and buyer power to motivate companies to disclose and manage their environmental impacts. Over 6,300 companies with some 55% of global market capitalization disclosed environmental data through CDP in 2017. This is in addition to the over 500 cities and 100 states and regions who disclosed, making CDP’s platform one of the richest sources of information globally on how companies and governments are driving environmental change. CDP, formerly Carbon Disclosure Project, is a founding member of the We Mean Business Coalition. Please visit www.cdp.net or follow us @CDP to find out more.

The report

This research is part of a series of award winning in-depth sector analysis by CDP to provide investors with the most comprehensive environmental data analysis. It aims to identify the most material metrics for each specific sector and how they link to financial performance. Our methodology is unique as the weighting assigned to each metric is transparent and can be applied individually according to investor preferences. These rankings are not intended to identify definitive winners and losers for investment purposes, but rather to indicate strategic advantage in an industry where there is a significant regulatory impact on all major markets.

Reports on the oil & gas, steel, cement, automotive, electric utilities, chemicals and mining industries were released in 2015, 2016, and 2017.

[1] Extel IRRI Survey 2017, 2016, 2015

[2] Operational emissions and materials used

[3] Fly ash and steel used, sourced from other carbon intensive sectors such as thermal power generation and steel production

Cement is the second most polluting industrial sector and is used in concrete, which after water is the most consumed product in the world. The built environment, which includes offices and residential buildings, uses concrete extensively and accounts for over a third of global emissions[2]. Regulation of the sector so far has been light but rising ambitions for low carbon cities and tightening building regulations could drive change up the chain.

Indian companies top the CDP league table thanks to reducing their carbon footprint during the cement making process, in part due to better access to alternative materials[3] from other carbon intensive sectors. They also benefit from newer and more efficient cement plants driven by high market growth in the region, in contrast to their European peers that rely on older cement plants.

Paul Simpson, CEO of CDP commented: “Cement is a heavy and largely invisible polluter, yet taken for granted as a necessary building block of basic civilization. With potential pressure coming from multiple sources, including down the value chain in the form of building and city regulation, cement companies need to invest and innovate in order to avoid impending risks to their operations and the wider world. This may seem challenging at first, but every year it is delayed, the cost becomes greater, so management teams, regulators and investors need to think long term. There is a solution - cement companies just need to invest properly in finding it.”

There are however opportunities for companies who act early on climate risk. Companies can reduce costs by making their cement plants more energy efficient and secure their position in future sustainable cement markets by investing in low-carbon products. Governments can facilitate the development of these markets through regulation and incentives.

The report also highlights other potential risks and opportunities for the sector:

- Carbon Capture and Storage (CCS) is an important technology for creating low-carbon cement yet CCS projects are still largely at pilot stage in the sector. Heidelberg shows some investment in CCS across various technologies, but otherwise progress is limited.

- European players benefit from alternative fuels sourced from organized waste collection, which becomes the fuel source for cement production. Emerging market producers are behind on this, due to limited infrastructure.

- Five companies do not use an internal carbon price, which is a significant risk in a sector where carbon pricing legislation could have a material impact.

- Carbon regulation such as the EU’s Emissions Trading Scheme is the key mechanism to regulate emissions from the sector in Europe. However, structural issues and lobbying of policymakers have undermined the potential for change for the sector.

- Cement companies are not incentivizing long-term climate risk management through executive level remuneration, with only Cementos Argos including this.

The CDP report assesses companies across four key areas aligned with the recommendations from Mark Carney’s Task Force on Climate-related Financial Disclosures (TCFD). As the TCFD recommendations become mainstream, investors will increasingly expect cement companies to disclose how they are adjusting their business models to manage transition risks, while taking advantage of the opportunity to generate revenue from the global transition to a low-carbon economy.

CDP’s summary League Table for cement companies is below:

Marco Kisic, Senior Analyst at CDP commented: “Cement companies have made some progress towards reducing their emissions, but they need to do a huge amount more. It is clearly a complicated story because of our global reliance on cement, and the inherent emissions of the sector, but there are things that can be done. Cement companies should be looking at ways to further use alternative materials and fuels, improve the energy efficiency of their plants, and accelerate investments in low-carbon technologies such as carbon capture and storage, which is crucial for their long-term viability. Regulation may be the key driver for change here, and interestingly this may come from downstream as building regulators and owners shift their focus from operational emissions, to those associated with creating the buildings themselves.”

Anhui Conch, Siam Cement, Dangote Cement and China National Building Materials did not respond to CDP’s 2017 climate change questionnaire and are therefore not included in this report. We encourage investors to raise this lack of transparency in discussions with company management.

You can view the executive summary of the report here.

About CDP and this report

About CDP

CDP is an international non-profit that drives companies and governments to reduce their greenhouse gas emissions, safeguard water resources and protect forests. Voted number one climate research provider by investors and working with institutional investors with assets of US$87 trillion, we leverage investor and buyer power to motivate companies to disclose and manage their environmental impacts. Over 6,300 companies with some 55% of global market capitalization disclosed environmental data through CDP in 2017. This is in addition to the over 500 cities and 100 states and regions who disclosed, making CDP’s platform one of the richest sources of information globally on how companies and governments are driving environmental change. CDP, formerly Carbon Disclosure Project, is a founding member of the We Mean Business Coalition. Please visit www.cdp.net or follow us @CDP to find out more.

The report

This research is part of a series of award winning in-depth sector analysis by CDP to provide investors with the most comprehensive environmental data analysis. It aims to identify the most material metrics for each specific sector and how they link to financial performance. Our methodology is unique as the weighting assigned to each metric is transparent and can be applied individually according to investor preferences. These rankings are not intended to identify definitive winners and losers for investment purposes, but rather to indicate strategic advantage in an industry where there is a significant regulatory impact on all major markets.

Reports on the oil & gas, steel, cement, automotive, electric utilities, chemicals and mining industries were released in 2015, 2016, and 2017.

[1] Extel IRRI Survey 2017, 2016, 2015

[2] Operational emissions and materials used

[3] Fly ash and steel used, sourced from other carbon intensive sectors such as thermal power generation and steel production

Author

Parul Dubey

Video: New Roundabout Under Construction at McIver and Old Florence Roads in Darlington County

K2b Cantonal Highway

June Issue 2026

.jpg?width=225)