In my experience, the top three reasons why A/E firms implement employee stock ownership plans (ESOPs) are taxes, taxes and taxes. However, although mitigating taxes is an important element, a good ownership plan should be driven by a firm’s strategic plan and long-term goals, which may include aligning ownership with leadership, making the investment process affordable to new owners, and ensuring that the stock produces a healthy return on investment for all owners. The tax consequences of an ownership plan should be considered in the context of how they impact the firm’s ability to achieve its strategic ownership goals.

Additional Options

ESOPs have long been considered the “panacea of tax efficiency” when it comes to ownership transition, but not every firm is a good candidate for ESOP ownership, particularly if it doesn’t address the firm’s strategic ownership goals. A few years ago, I created an ownership model that has economic benefits similar to those of an ESOP, but not as costly in implementing and operating nor requiring ownership to be shared with all employees.

This model uses common and synthetic securities, with the former being valued at adjusted book value, and the latter having a value similar to the goodwill value of the firm. On a combined basis, the value of these two securities will be similar to the company’s fair market value. The tax benefits of this plan can be significant, especially if your firm is very profitable. The key difference is that a shareholder will buy shares and earn their synthetic equity.

Charting Scenarios

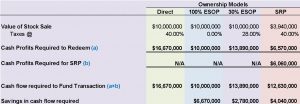

The accompanying table demonstrates four ownership transition scenarios as well as a comparison of the required cash flow to redeem the same volume shares under each scenario. These are actual metrics of a client.

In the example, the company’s book value is $3.94 million, its fair market value is $10 million, and the assumed tax rate is 40 percent. We have compared the economic benefit of redeeming $10 million of value using a direct ownership model, a 100 percent ESOP ownership model, a 30 percent ESOP ownership model, and a Supplemental Retirement Plan (SRP) model, which uses common and synthetic equity.

The cost of redeeming $10 million in stock under the direct ownership model is $16.67 million, because the company has to generate enough profits to pay taxes so it has $10 million left over to redeem the shares (net income/[1-tax rate]). Under a 100 percent ESOP model, the company would only have to generate $10 million in profits, because at 100 percent ESOP ownership, the company becomes a tax-free entity and isn’t subject to corporate taxes (the company is a subchapter S corporation). This savings significantly enhances the overall liquidity of the shares because of the tax efficiencies, which is why we’ve seen so many firms consider a 100 percent ESOP ownership model.

Under a 30 percent ESOP model, the company would have to generate $13.89 million in profits, paying taxes of $3.89 million, to have $10 million remaining to redeem the shares. This explains why many firms adopt the partial ESOP ownership model. Although the benefits aren’t as great as the 100 percent ESOP, it still represents significant tax savings over the direct ownership model.

Now let’s consider the SRP model. Assuming the shares are redeemed at book value and SRP units are redeemed at the difference between $10 million and $3.94 million ($6.57 million), the total cash flow required is $12.63 million. This is lower than the Direct and 30 percent ESOP models, because the SRP units are tax deductible to the company (this security instrument takes on similar features to a deferred compensation plan). In addition, the SRP model has some key benefits that go beyond the aforementioned tax benefits. For example, creating an attractive return on investment now is easier because lower cash flow is required to yield greater returns.

In this example, the company pays a 15 percent dividend on its common stock. At book value, the total dividend paid is $591,000. This makes the investment in common equity extremely attractive. Because the SRP component of this model can be a significant portion of the overall value to a shareholder, it’s advisable that the SRP units vest over a long period of time, encouraging long-term commitment on the part of shareholders.

Michael O'Brien

Michael S. O’Brien is a principal in the Washington, D.C., office of Rusk O’Brien Gido + Partners, specializing in corporate financial advisory services including business valuation, fairness and solvency opinions, mergers and acquisitions, internal ownership transition consulting, ESOPs, and strategic planning; email: [email protected].

Video: New Roundabout Under Construction at McIver and Old Florence Roads in Darlington County

Bridge Replacement at Amsterdam Centraal Station

June Issue 2026

.jpg?width=225)